The Fokker-Planck forward equation is an important tool to calibrate local volatility extensions of stochastic volatility models, e.g. the local vol extension of the Heston model. But the treatment of the boundary conditions – especially at zero instantaneous variance – is notoriously difficult if the Feller constraint

of the square root process for the variance

is violated. The corresponding Fokker-Planck forward equation

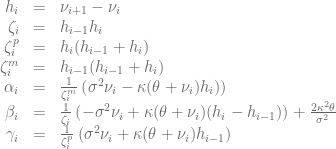

describes the time evolution of the probability density function p and the boundary at the origin

diverges with

and the zero flow boundary condition at the origin

![\left.\left[ \frac{\sigma^2}{2}\frac{\partial}{\partial \nu} (\nu p) + \kappa(\nu-\theta)p\right]\right|_{\nu=0} = 0](https://s0.wp.com/latex.php?latex=%5Cleft.%5Cleft%5B+%5Cfrac%7B%5Csigma%5E2%7D%7B2%7D%5Cfrac%7B%5Cpartial%7D%7B%5Cpartial+%5Cnu%7D+%28%5Cnu+p%29+%2B+%5Ckappa%28%5Cnu-%5Ctheta%29p%5Cright%5D%5Cright%7C_%7B%5Cnu%3D0%7D+%3D+0+&bg=ffffff&fg=5e5e5e&s=0&c=20201002)

becomes hard to track numerically. Rewriting the partial differential equation in terms of

The corresponding zero flow boundary condition in q reads as follows

![\left.\left[ \nu\frac{\sigma^2}{2}\frac{\partial}{\partial \nu} q + \kappa\nu q\right]\right|_{\nu=0} = 0](https://s0.wp.com/latex.php?latex=%5Cleft.%5Cleft%5B+%5Cnu%5Cfrac%7B%5Csigma%5E2%7D%7B2%7D%5Cfrac%7B%5Cpartial%7D%7B%5Cpartial+%5Cnu%7D+q+%2B+%5Ckappa%5Cnu+q%5Cright%5D%5Cright%7C_%7B%5Cnu%3D0%7D+%3D+0+&bg=ffffff&fg=5e5e5e&s=0&c=20201002)

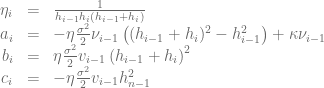

The first step in order to apply the boundary condition is to discretize the transformed Fokker-Planck equation in space direction on a non-uniform grid

![\frac{\partial q_i}{\partial t} = \alpha_iq_{i-1}+\beta_iq_i+\gamma_iq_{i+1]}](https://s0.wp.com/latex.php?latex=%5Cfrac%7B%5Cpartial+q_i%7D%7B%5Cpartial+t%7D+%3D+%5Calpha_iq_%7Bi-1%7D%2B%5Cbeta_iq_i%2B%5Cgamma_iq_%7Bi%2B1%5D%7D+&bg=ffffff&fg=5e5e5e&s=0&c=20201002)

with

Next step is to discretize the zero flow boundary condition using a second order forward discretization [3] for the derivative

![\left.\left[ \nu\frac{\sigma^2}{2}\frac{\partial}{\partial \nu} q + \kappa\nu q\right]\right|_{\nu=\nu_{i-1}} \approx a_iq_{i-1} + b_iq_{i} + c_iq_{i+1} = 0](https://s0.wp.com/latex.php?latex=%5Cleft.%5Cleft%5B+%5Cnu%5Cfrac%7B%5Csigma%5E2%7D%7B2%7D%5Cfrac%7B%5Cpartial%7D%7B%5Cpartial+%5Cnu%7D+q+%2B+%5Ckappa%5Cnu+q%5Cright%5D%5Cright%7C_%7B%5Cnu%3D%5Cnu_%7Bi-1%7D%7D+%5Capprox+a_iq_%7Bi-1%7D+%2B+b_iq_%7Bi%7D+%2B+c_iq_%7Bi%2B1%7D+%3D+0+&bg=ffffff&fg=5e5e5e&s=0&c=20201002)

with

Now the value

This equation can be used to remove the boundary value

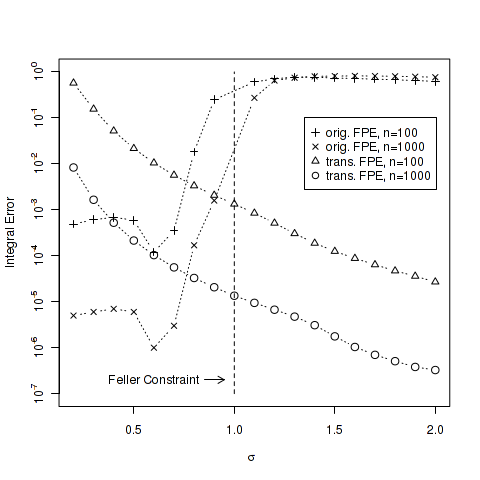

The following parameters of the square-root process will be used to test the different boundary conditions.

The uniform grid

The grid covers 98% of the distribution and this value would not change over time if the boundary conditions are satisfied without discretiszation errors. To test the magnitude of the discretization errors we let the initial solution evolve over one year using 100 time steps with the Crank-Nicolson scheme. The resulting solution

servers as a quality indicator for the discretization errors of the boundary condition.

As can be seen in the diagram below if

The same techniques can be used to solve the Fokker-Planck equation for the Heston model. The code for the numerical tests is available in the latest QuantLib version from the SVN trunk. The diagram is based on the test FDHestonTest::testSquareRootEvolveWithStationaryDensity.

[1] A. Dragulescu, V. Yakovenko, Probability distribution of returns in the Heston model with stochastic volatility

[2] V. Lucic, Boundary Conditions for Computing Densities in Hybrid Models via PDE Methods

[3] P. Lermusiaux, Numerical Fluid Mechanics, Lecture Note 14, Page 5

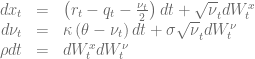

denotes the Dirac delta distribution. A semi-closed form solution for this problem is presented in [1]. When solving the Fokker-Planck forward equation special care must be taken with respect to the boundary conditions, especially if the Feller constraint

denotes the Dirac delta distribution. A semi-closed form solution for this problem is presented in [1]. When solving the Fokker-Planck forward equation special care must be taken with respect to the boundary conditions, especially if the Feller constraint is instantaneously attainable. A generalisation of Feller’s zero-flux boundary condition should be applied at the origin [2].

is instantaneously attainable. A generalisation of Feller’s zero-flux boundary condition should be applied at the origin [2].![\left.\left[ \frac{\sigma^2}{2}\frac{\partial}{\partial \nu} (\nu p) + \kappa(\nu-\theta)p + \rho\nu\sigma\frac{\partial p}{\partial x}\right]\right|_{\nu=0} = 0, \ \forall x\in \mathbb{R}^+](https://s0.wp.com/latex.php?latex=%5Cleft.%5Cleft%5B+%5Cfrac%7B%5Csigma%5E2%7D%7B2%7D%5Cfrac%7B%5Cpartial%7D%7B%5Cpartial+%5Cnu%7D+%28%5Cnu+p%29+%2B+%5Ckappa%28%5Cnu-%5Ctheta%29p+%2B+%5Crho%5Cnu%5Csigma%5Cfrac%7B%5Cpartial+p%7D%7B%5Cpartial+x%7D%5Cright%5D%5Cright%7C_%7B%5Cnu%3D0%7D+%3D+0%2C+%5C+%5Cforall+x%5Cin+%5Cmathbb%7BR%7D%5E%2B+&bg=ffffff&fg=5e5e5e&s=0&c=20201002)

for

for  [3].

[3].

and this changes the shape of the solution completely.

and this changes the shape of the solution completely.

for typical partial differential equations in financial engineering. Unfortunately if these schemes are used together with dynamic programming to price America options the second order convergence is destroyed by the first order convergence of the dynamic programming step.

for typical partial differential equations in financial engineering. Unfortunately if these schemes are used together with dynamic programming to price America options the second order convergence is destroyed by the first order convergence of the dynamic programming step. .

. does not depend on

does not depend on

is n+1. The order does not depend on the particular value of x but often x is chosen to be two. This simple trick can be extended to the case where n is unknown or the Richardson extrapolation can be used m times to increase the order of convergence to n+m [2].

is n+1. The order does not depend on the particular value of x but often x is chosen to be two. This simple trick can be extended to the case where n is unknown or the Richardson extrapolation can be used m times to increase the order of convergence to n+m [2].

.

.

anyhow. This step size is small enough for the implicit Euler scheme to obtain a very good accuracy. The explicit Euler scheme is numerically unstable, even if

anyhow. This step size is small enough for the implicit Euler scheme to obtain a very good accuracy. The explicit Euler scheme is numerically unstable, even if  and

and  .

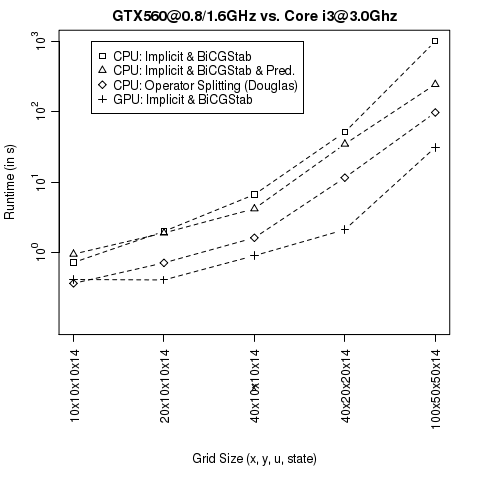

. operations. The corresponding preconditioner can be seen as a natural extension of the diagonal preconditioner. Experiments on a CPU indicate that the tridiagonal preconditioner leads to a significant speed-up for our VPP pricing problem. The upcoming CUSPARSE library of the

operations. The corresponding preconditioner can be seen as a natural extension of the diagonal preconditioner. Experiments on a CPU indicate that the tridiagonal preconditioner leads to a significant speed-up for our VPP pricing problem. The upcoming CUSPARSE library of the  and a maturity of 4 weeks (corresponds to

and a maturity of 4 weeks (corresponds to  exercise steps). Therefore in addition to the three dimensions for the stochastic model the problem has a fourth dimension of size

exercise steps). Therefore in addition to the three dimensions for the stochastic model the problem has a fourth dimension of size  to solve the optimization problem via dynamic programming.

to solve the optimization problem via dynamic programming.

is denoting the market instantaneous forward rate at time 0 for the maturity T (see. e.g. [1]). The Hull-White model can be seen as a one-dimensional simplification of the G2++ model. The corresponding partial differential equation (PDE) can be derived using the

is denoting the market instantaneous forward rate at time 0 for the maturity T (see. e.g. [1]). The Hull-White model can be seen as a one-dimensional simplification of the G2++ model. The corresponding partial differential equation (PDE) can be derived using the

operations instead of

operations instead of  operations required by the Gaussian elimination. But it is not easy to parallelize the Thomas algorithm.

operations required by the Gaussian elimination. But it is not easy to parallelize the Thomas algorithm.

![\begin{array}{|c|c|c|c|c|c|c|c|c|} \hline {\rm Model} & v_0 & \kappa_v & \theta_v & \sigma_v & \rho_{Sv} & r & q & \mbox{Ref} \\ \hline \hline {\rm't\ Hout\ Case\ 1}& 0.04& 1.5& 0.04& 0.3& -0.9& 0.025& 0.0 &[2]\\ {\rm't\ Hout\ Case\ 2} & 0.12& 3.0& 0.12& 0.04& 0.6& 0.01& 0.04 &[2]\\ {\rm't\ Hout\ Case\ 3}& 0.0707&0.6067& 0.0707& 0.2928& -0.7571& 0.03& 0.0 & [2]\\ {\rm't\ Hout\ Case\ 4}& 0.06& 2.5& 0.06& 0.5& -0.1& 0.0507& 0.0469 &[2]\\ {\rm Ikonen\ Toivanen}& 0.0625& 5& 0.16& 0.9& 0.1& 0.1& 0.0 &[3]\\ {\rm Kahl\ J\ddot{a}ckel}& 0.16& 1.0& 0.16& 2.0& -0.8& 0.0& 0.0 &[4]\\ {\rm Equity Case }& 0.07& 2.0& 0.04& 0.55& -0.8& 0.03& 0.035 &\\ {\rm High Correlation}& 0.07& 1.0& 0.04& 0.55& 0.9& 0.02& 0.04& \\ {\rm small\ \sigma_v}& 0.07& 1.0& 0.04& 0.001& -0.75& 0.04& 0.03& \\ \kappa_v=\sigma_v\rho_{Sv}& 0.07& 0.4& 0.04& 0.5& 0.8& 0.03& 0.03 &\\ \hline \end{array}](https://s0.wp.com/latex.php?latex=%5Cbegin%7Barray%7D%7B%7Cc%7Cc%7Cc%7Cc%7Cc%7Cc%7Cc%7Cc%7Cc%7C%7D+%5Chline+%7B%5Crm+Model%7D+%26+v_0+%26+%5Ckappa_v+%26+%5Ctheta_v+%26+%5Csigma_v+%26+%5Crho_%7BSv%7D+%26+r+%26+q+%26+%5Cmbox%7BRef%7D+%5C%5C+%5Chline+%5Chline+%7B%5Crm%27t%5C+Hout%5C+Case%5C+1%7D%26+0.04%26+1.5%26+0.04%26+0.3%26+-0.9%26+0.025%26+0.0+%26%5B2%5D%5C%5C+%7B%5Crm%27t%5C+Hout%5C+Case%5C+2%7D+%26+0.12%26+3.0%26+0.12%26+0.04%26+0.6%26+0.01%26+0.04+%26%5B2%5D%5C%5C+%7B%5Crm%27t%5C+Hout%5C+Case%5C+3%7D%26+0.0707%260.6067%26+0.0707%26+0.2928%26+-0.7571%26+0.03%26+0.0+%26+%5B2%5D%5C%5C+%7B%5Crm%27t%5C+Hout%5C+Case%5C+4%7D%26+0.06%26+2.5%26+0.06%26+0.5%26+-0.1%26+0.0507%26+0.0469+%26%5B2%5D%5C%5C+%7B%5Crm+Ikonen%5C+Toivanen%7D%26+0.0625%26+5%26+0.16%26+0.9%26+0.1%26+0.1%26+0.0+%26%5B3%5D%5C%5C+%7B%5Crm+Kahl%5C+J%5Cddot%7Ba%7Dckel%7D%26+0.16%26+1.0%26+0.16%26+2.0%26+-0.8%26+0.0%26+0.0+%26%5B4%5D%5C%5C+%7B%5Crm+Equity+Case+%7D%26+0.07%26+2.0%26+0.04%26+0.55%26+-0.8%26+0.03%26+0.035+%26%5C%5C+%7B%5Crm+High+Correlation%7D%26+0.07%26+1.0%26+0.04%26+0.55%26+0.9%26+0.02%26+0.04%26+%5C%5C+%7B%5Crm+small%5C+%5Csigma_v%7D%26+0.07%26+1.0%26+0.04%26+0.001%26+-0.75%26+0.04%26+0.03%26+%5C%5C+%5Ckappa_v%3D%5Csigma_v%5Crho_%7BSv%7D%26+0.07%26+0.4%26+0.04%26+0.5%26+0.8%26+0.03%26+0.03+%26%5C%5C+%5Chline+%5Cend%7Barray%7D&bg=ffffff&fg=5e5e5e&s=0&c=20201002)

and

and  . The equity interest rate correlation is

. The equity interest rate correlation is  , interest rates and stochastic volatility aren’t correlated

, interest rates and stochastic volatility aren’t correlated  The benchmark call options have maturity of 5 years, underlying at time

The benchmark call options have maturity of 5 years, underlying at time  is

is  and possible strikes are

and possible strikes are .

. strikes and

strikes and  models.

models.

. and with control variate based on the semi–closed Heston Model. Clearly the Douglas scheme is the worst performer, the (modified) Craig-Sneyd and modified Hundsdorfer-Verwer scheme are the winner.

. and with control variate based on the semi–closed Heston Model. Clearly the Douglas scheme is the worst performer, the (modified) Craig-Sneyd and modified Hundsdorfer-Verwer scheme are the winner.

![\begin{array}{rcl} rV&=&\frac{\partial V}{\partial t}+\frac{\sigma_x^2}{2}\frac{\partial^2 V}{\partial x^2}-\alpha x\frac{\partial V}{\partial x}-\beta y \frac{\partial V}{\partial y} \\[6pt]&+&\frac{\sigma_u^2}{2}\frac{\partial^2 V}{\partial u^2}- \kappa u\frac{\partial V}{\partial u} +\rho\sigma_x\sigma_u\frac{\partial^2 V}{\partial x\partial u}\\[6pt] &+&\lambda\int_\mathbb{R}\left(V(x,y+z,u,t)-V(x,y,u,t) \right )\omega(z)dz \\ \end{array}](https://s0.wp.com/latex.php?latex=%5Cbegin%7Barray%7D%7Brcl%7D+rV%26%3D%26%5Cfrac%7B%5Cpartial+V%7D%7B%5Cpartial+t%7D%2B%5Cfrac%7B%5Csigma_x%5E2%7D%7B2%7D%5Cfrac%7B%5Cpartial%5E2+V%7D%7B%5Cpartial+x%5E2%7D-%5Calpha+x%5Cfrac%7B%5Cpartial+V%7D%7B%5Cpartial+x%7D-%5Cbeta+y+%5Cfrac%7B%5Cpartial+V%7D%7B%5Cpartial+y%7D+%5C%5C%5B6pt%5D%26%2B%26%5Cfrac%7B%5Csigma_u%5E2%7D%7B2%7D%5Cfrac%7B%5Cpartial%5E2+V%7D%7B%5Cpartial+u%5E2%7D-+%5Ckappa+u%5Cfrac%7B%5Cpartial+V%7D%7B%5Cpartial+u%7D+%2B%5Crho%5Csigma_x%5Csigma_u%5Cfrac%7B%5Cpartial%5E2+V%7D%7B%5Cpartial+x%5Cpartial+u%7D%5C%5C%5B6pt%5D+%26%2B%26%5Clambda%5Cint_%5Cmathbb%7BR%7D%5Cleft%28V%28x%2Cy%2Bz%2Cu%2Ct%29-V%28x%2Cy%2Cu%2Ct%29+%5Cright+%29%5Comega%28z%29dz+%5C%5C+%5Cend%7Barray%7D&bg=ffffff&fg=5e5e5e&s=0&c=20201002)

has

has  different states.

different states.

.

. exercise opportunities. The number of overall exercised swing opportunities is constraint by

exercise opportunities. The number of overall exercised swing opportunities is constraint by .

.

{kind=link}

{kind=link}

{kind=link}

{kind=link}