Despite being based on a fairly simple stochastic differential equation

the corresponding partial differential equation

for the SABR model – derived using the variable transformation

and assume absorbing boundary conditions at

Please notice that the underlying

![F_t= \left[{t \left({\chi'}^2\right)}^{-1} \left(1-q; \delta, \frac{X_0}{t}\right) \alpha^2(1-\beta)^2\right]^{\frac{1}{2(1-\beta)}}](https://s0.wp.com/latex.php?latex=F_t%3D+%5Cleft%5B%7Bt+%5Cleft%28%7B%5Cchi%27%7D%5E2%5Cright%29%7D%5E%7B-1%7D+%5Cleft%281-q%3B+%5Cdelta%2C+%5Cfrac%7BX_0%7D%7Bt%7D%5Cright%29%C2%A0+%5Calpha%5E2%281-%5Cbeta%29%5E2%5Cright%5D%5E%7B%5Cfrac%7B1%7D%7B2%281-%5Cbeta%29%7D%7D&bg=ffffff&fg=5e5e5e&s=0&c=20201002)

which can be computed using the boost library. In addition adaptive grid refinement around important points and cell averaging around special points of the payoff at maturity [3] improve the accuracy of the CEV finite difference scheme.

and acts as a litmus test for the implementation of the boundary conditions and the finite difference scheme.

The variance direction

The finite difference solver can now be used to compare different approximations with the correct model behaviour and also to compare it with high accurate Monte-Carlo simulations [2]. The model configuration [5]

should act as a test bed. As can be seen in the diagram below the Monte-Carlo results are in line with the results from finite difference methods within very small error bars. The standard Hagan et al. formula as well as the Le Floc’h-Kennedy [6] log-normal formula deviate significantly from the correct implied volatilities.

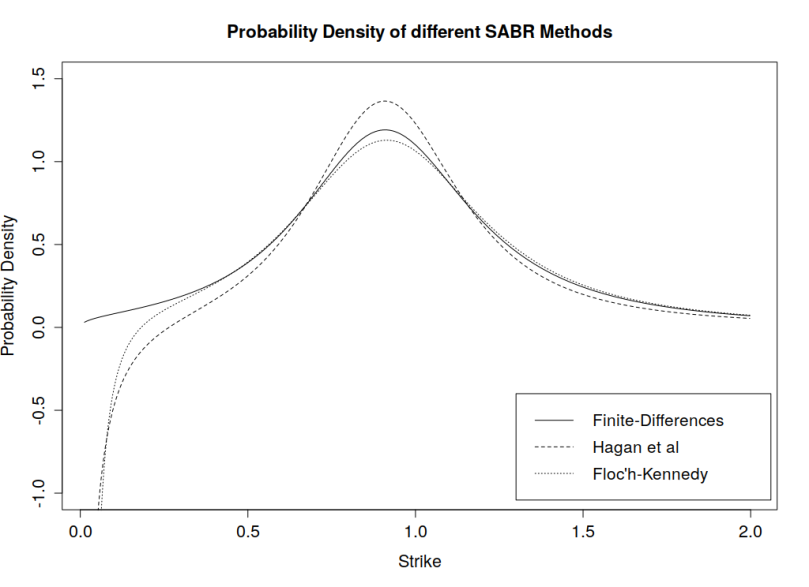

The approximations are not arbitrage free. The probability densities for small strikes turn negative. Hagan’s formula exhibits this behaviour already for larger strikes than the Le Floc’h-Kennedy formula as can be seen in the following diagram. As expected the finite difference solution does not produce negative probabilities.

A note on the Floc’h-Kennedy approximation, the formula becomes numerically unstable around ATM strike levels, hence a second order Taylor expansion is used for moneyness

A note on the Floc’h-Kennedy approximation, the formula becomes numerically unstable around ATM strike levels, hence a second order Taylor expansion is used for moneyness

The following diagram shows the difference between second order Taylor expansion and the formula evaluated using IEEE-754 double precision.

The source code is part of the PR #589 and available here.

[1] D.R. Brecher, A.E. Lindsay: Results on the CEV Process, Past and Present.

[2] B. Chen, C.W. Oosterlee, H. Weide, Efficient unbiased simulation scheme for the SABR stochastic volatility model.

[3] K. in’t Hout: Numerical Partial Differential Equations in Finance explained.

[4] K. in’t Hout, S. Foulon: ADI Finite Difference Schemes for Option Pricing in the Heston Model with Correlation.

[5] P. Hagan, D. Kumar, A. Lesnieski, D. Woodward: Arbitrage free SABR.

[6] F. Le Floc’h, G. Kennedy: Explicit SABR Calibration through Simple Expansions.